What does it consist of?

It consists of an accounting of the income (credit) and expenses (debit) of the cash-on-hand.

Who should take charge of it?

The fidelity and continuity of this confidential work must be placed in the hands of the treasurers to whom the administration of the money of the Association is entrusted. This accounting permits the verification of the correct use of the goods of the Association. As such, it should be applied at all organizational levels: national, provincial, regional and local.

How is it done?

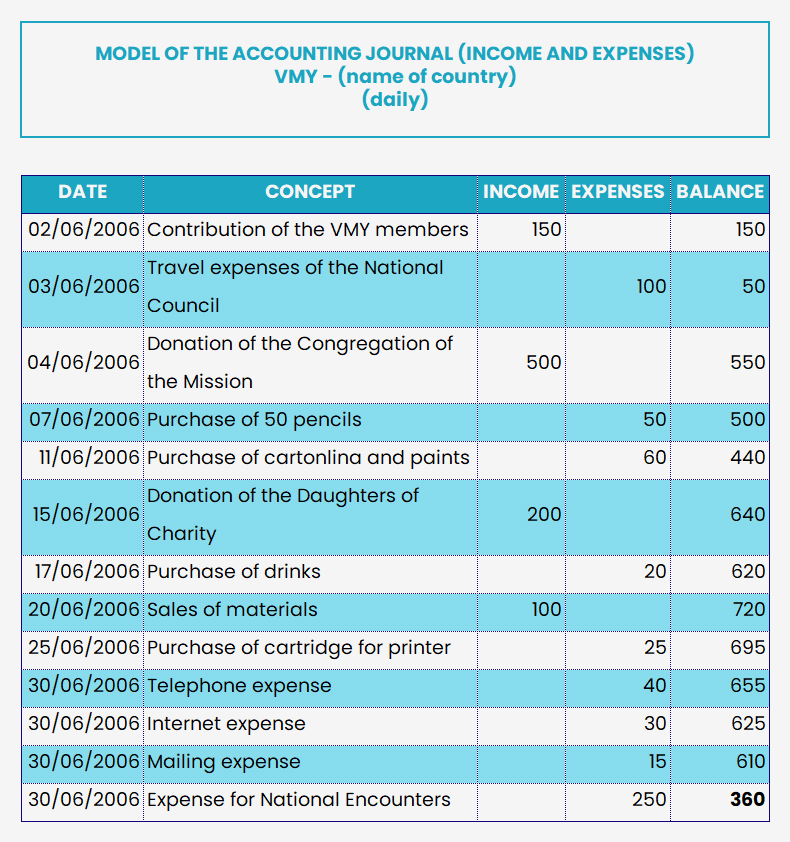

The accounting of expenses and cash income will be done periodically and chronologically. It is recommended to put in the item or concept box all the descriptions in a specific manner in order to explain how the money was used. This practice needs discipline and continuity in order to update the expenses and revenues, savings, donations, contributions of the members, etc.

The person-in-charge of the accounting must always ask for and submit supporting documents or receipts that specify the value of the expense or deposit made. These documents should be filed in a chronological order so that they can be easily referenced when needed and when filing reports.

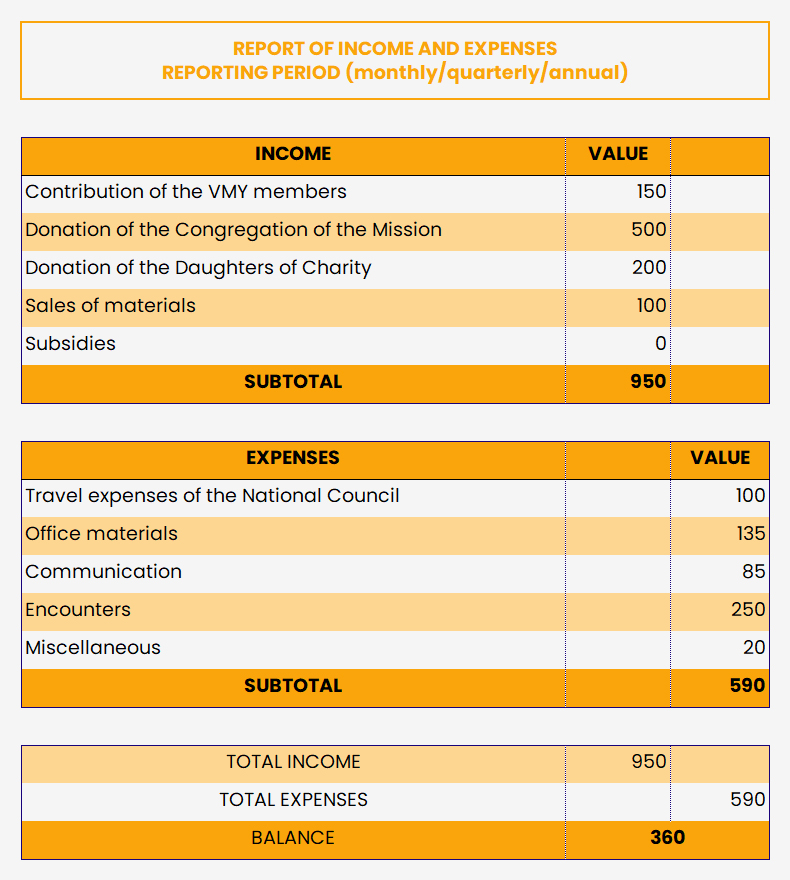

The treasurer shall prepare the annual report, (this is a compilation of the monthly and quarterly reports) which is to be presented to the National Council and all competent entities mentioned in the National Statutes.

The result of the annual report reveals the remaining balance. If the income is more than the expenses, there will be a surplus of funds (money in one’s favor); if the balance is negative, there shall be a deficit and debts to be paid. In this case the budget has to be revised and the financial situation of the Association has to be analyzed.

The treasurer will send a copy of the annual report to the Director of the International Secretariat; this should be considered confidential document. (Financial Determinations – 1st General Assembly, Rome 2000).

We present below a model of the report to be used.

For purposes of good management, it is advisable that an annual inventory of the assets (furniture, etc.) and properties of the Association be made.

It is necessary to keep a file of the documents that prove that the goods are the Association’s property as well as a register of the payments made to the State (taxes) and the expenses incurred for the maintenance of the said goods.

It is advisable to create a commission which advises the National Council in the management of these goods.

These funds are intended to provide a stable financial support to the Association. They will generate new resources that that can be utilized in the different activities. It is recommended to deposit this money in the bank.

Ratifying the commitments of the 1st General Assembly Rome 2000 (Accounting Guidelines Art. 2) let us remember that “the bank accounts of the National Councils should be in the name of the Association, with the necessary legal registrations as well as the signature and supervision of the National Adviser.”

The National Council will draft a document which determines the manner of managing and increasing this fund in accord with the financial situation of the country.

Article 5.3.1 of the Final Document of the 2nd General Assembly Paris 2005 states that, “We ratify all the economic commitments of the General Assembly of Rome 2000, especially the process of annual contributions from each member country which help defray the expenses of the coordinating group. All the local centers and each member must contribute in order to achieve this reality of self-sufficiency.” The National Council must make the members aware of their responsibility to contribute to the economic maintenance of the Association.

Once the membership fees have been collected, the National Council will allocate these funds according to the responsibilities that it has incurred (International Secretariat, Vincentian Family Councils, Church Organizations, etc.).

The National Treasurer shall organize campaign drives on the different organizational levels of the Association to promote self-financing.

The National Councils shall look for ways to obtain subsidies from public and private organizations within their own country. For this, however, the civil recognition of the Association is needed.